A few years ago, I used to think wealth building was something only financially smart or rich people could do. But by 2025, I realized that smart money moves actually start with simple things—small steps that anyone can take. The journey wasn’t easy for me either. I was also the person who would open the shopping cart as soon as the salary arrived. But when I started tracking my spending, improved my financial habits, and adopted long-term thinking—that’s when my finances slowly began to change.

Today, I can say from my experience that wealth building is not tough; it just requires discipline and clarity.

In this blog, I am sharing the smart money moves that I personally followed and whose results I clearly started seeing in 2024-2025.

1. Tracking Spending: The Simplest and Most Powerful Step

My biggest problem was that I didn’t even know where my money went.

I thought I didn’t spend much—but when I used a simple free expense tracker app last year, I was shocked. In just one week, I found out about:

- 4 times coffee

- 2 times random food delivery

- Unnecessary subscriptions

- Impulsive weekend shopping

The total? More than ₹6,000 wasted in a month.

The first step to a smart money move in 2025 is this: Track your spending.

I would take 2 minutes every day to log my expenses. This helped me figure out which habits were financially draining me. Trust me, this step was a game-changer for me.

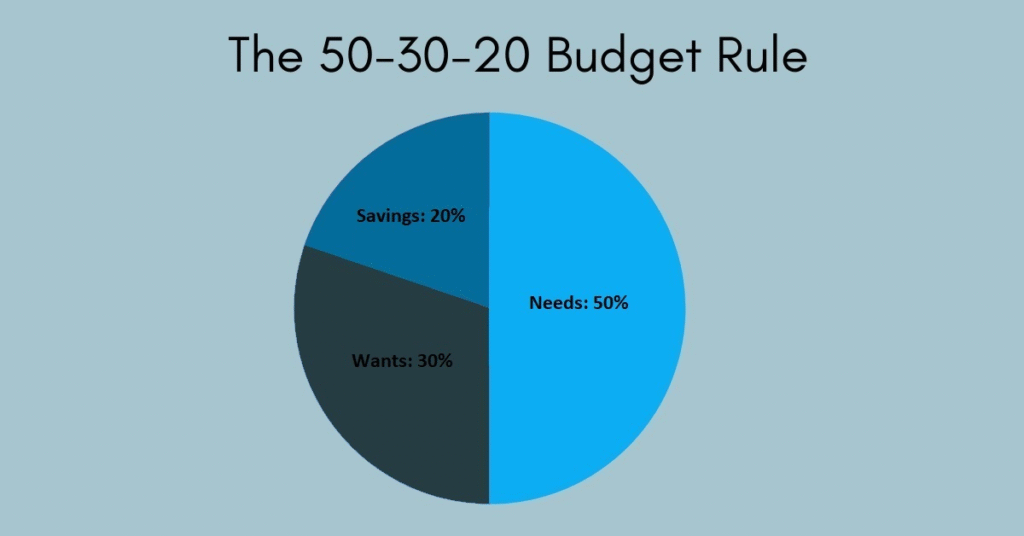

2. The 50-30-20 Rule: The Budget That Finally Worked

Before, I would try to budget, but after a day or two, I would forget.

But the 50-30-20 rule simplified my life:

- 50% – Needs: Rent, groceries, bills

- 30% – Wants: Dining out, entertainment

- 20% – Savings/Investments

This gave me clarity on how much I should save every month without burdening my lifestyle. In the time of inflation in 2025, this rule is still practical; it just requires a little adjustment.

Sometimes, my ‘Wants’ part goes from 30 to 20, and ‘Saving’ goes from 20 to 30—depending on my goals.

3. Creating an Emergency Fund: My Mental Peace Bank

In 2023, when an unexpected expense came up during my health checkup, I realized how important an emergency fund is. I only had ₹5,000 left then, and I had to borrow money from outside.

That’s when I decided that an emergency fund would now be compulsory.

My emergency fund goal for 2025 is: Keep 3–6 months of expenses in a separate account.

I started with just ₹500 per week. Slowly, it grew into a good amount.

Now I know that financial shocks can be handled without stress.

4. Starting Investment: Small Start, Big Difference

Earlier, I found investing risky. I thought the stock market was only for experts.

But when I started with an SIP—just ₹1,000 per month—I felt financially empowered.

My investment plan in 2024 was simple:

- Mutual Funds (SIP)

- Index Funds

- Digital Gold (very small portion)

In 2025, I am diversifying a bit:

- Blue-chip stocks (very carefully)

- More index funds

- High-interest savings account

My learning: Investing is not complicated; the mindset is complicated.

When you take small steps, your confidence automatically grows.

5. Canceling Useless Subscriptions: Small Step, Big Savings

There was a time when I had 9+ subscriptions—apps, OTT platforms, music, even a gaming app that I didn’t use.

When I listed all my subscriptions, I realized I was wasting ₹1,200 a month just on unused apps.

So I made a simple rule: If not used in 30 days — CANCEL.

This increased my annual savings by almost ₹12,000—without any effort.

6. Side Income: 2025’s Most Underrated Smart Money Move

I always thought that side income could only be generated by freelancers or influencers. But then I realized that anyone can create a side income. I personally tried this:

- Weekend online tasks

- Small content writing gigs

- Selling unused items

- Tutoring part-time

Even an extra ₹4,000–₹5,000 per month fast-tracked my savings goals. In 2025, creating a side income I think has become not optional but necessary—even if it’s small.

7. Using Credit Card Smartly

Earlier, I used to treat my credit card as “free money” (yes, a mistake!).

There was overspending, followed by guilt after seeing the bill.

In 2025, I only follow these rules:

- Full payment before the due date.

- Only use cashback cards.

- Only planned purchases.

This gives me reward points and also improves my credit score.

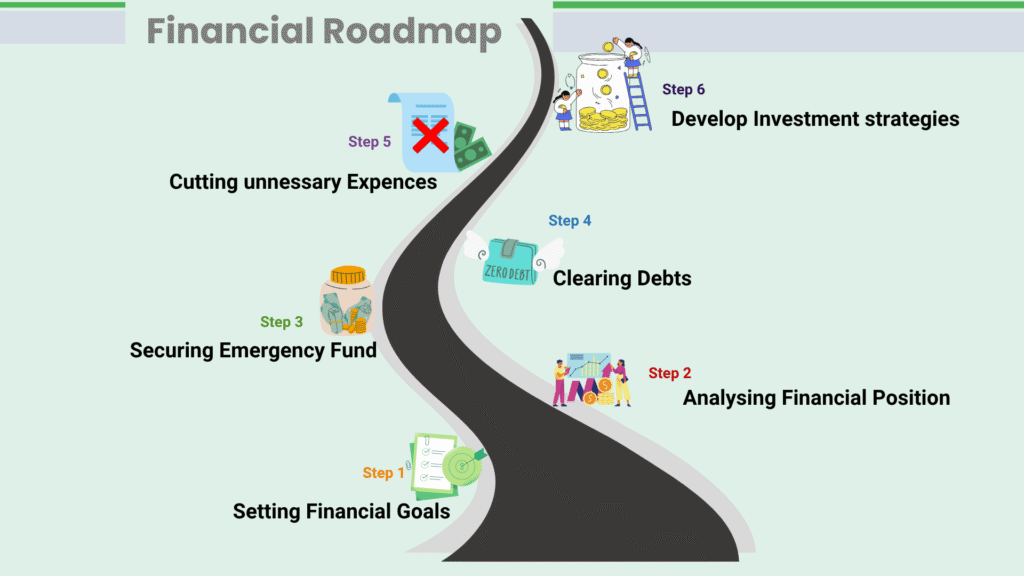

8. Creating Clear Financial Goals: The Roadmap That Worked for Me

Before, my goals were vague—”I need to save money.” But vague goals don’t provide motivation. Now my financial goals are clear, written, and achievable:

- ₹1 lakh emergency fund in 2025.

- ₹25k mutual fund investment by March.

- Vacation budget of ₹20k without loans.

- Increase income savings by 10% by year-end.

Clarity is power. When the target is clear, the action automatically gets sorted out.

Conclusion: Wealth Building Is a Journey, Not a Race

The meaning of wealth building changed for me in 2025. It’s not about earning more—it’s about managing better.If you are a beginner, just start with these 3 steps:

- Track your spending.

- Create a budget.

- Start an SIP (even with ₹500).

Small steps make the biggest difference.The smart money moves that seem small today will become the foundation of your financial stability in the future.

This blog is based purely on my personal experiences and understanding of money management. I am not a certified financial advisor. The strategies and suggestions shared here may not work the same way for everyone. Before making any financial decisions, please consider your personal situation or consult a professional financial expert. All information is for educational and motivational purposes only.

#SmartMoney2025#WealthBuildingTips#PersonalFinanceJourney#MoneyManagement2025#FinancialFreedomGoals#BudgetingMadeEasy #InvestingForBeginners#SavingsStrategies#FinanceBlog2025#WealthMindset#Carrerbook#Anslation